FTSE 100 FINISH LINE 16/4/26

FTSE 100 FINISH LINE 16/4/26

UK equities traded modestly higher on Thursday, with the major indices supported by strength in materials, financials, and construction-related names, as investors responded positively to renewed signs of possible de-escalation in the Middle East. Sentiment improved after President Trump said talks between Washington and Tehran were scheduled for Thursday, reinforcing hopes that the recent conflict may move toward a more stable diplomatic phase. The tone was broadly constructive across cyclicals, with investors also digesting stronger-than-expected domestic growth data. The materials sector was among the session’s better performers, helped by firmer base metal prices. Industrial metal miners rose around 0.8%, with Rio Tinto adding 1.6% and Anglo American up 1.3%, as the improvement in global risk appetite fed through into commodity-sensitive areas of the market.

On the macro front, UK data showed that the economy recorded its strongest monthly expansion in a year in February, providing an additional tailwind for domestically focused equities. At the same time, Bank of England Governor Andrew Bailey struck a measured tone in comments to the BBC, indicating that the Bank would not rush to raise interest rates in response to the latest energy shock. That combination—stronger activity data but no clear signal of imminent policy tightening— was broadly supportive for risk assets. The financial sector also contributed to the upside, as investors leveraged their preferred areas of the market to improve sentiment. Despite mixed performance within the space, 3i Group rose 1.4%. Ashmore fell 3.3% after reporting net outflows, reflecting ongoing pressure linked to volatility and uncertainty stemming from the US-Israel-Iran conflict.

In stock-specific moves, Morgan Sindall was the clear standout, surging 8% after upgrading its profit outlook. The update lifted sentiment across the broader construction and materials segment, which gained 2.2% on the day. Elsewhere, Tesco said its profit outlook had become more uncertain because of Middle East-related risks, though the market looked through the cautionary tone and sent the shares 1.13% higher. On the downside, EasyJet was among the notable laggards, falling 3.6% after warning that first-half losses would be wider than previously expected as the conflict continued to weigh on trading conditions and demand visibility. Overall, the session reflected a market still inclined to add risk as long as geopolitical headlines continue to move in a less threatening direction. Better UK activity data, steady central bank messaging, and support from commodity-linked sectors helped keep the tone constructive, even as investors remained selective at the single-stock level.

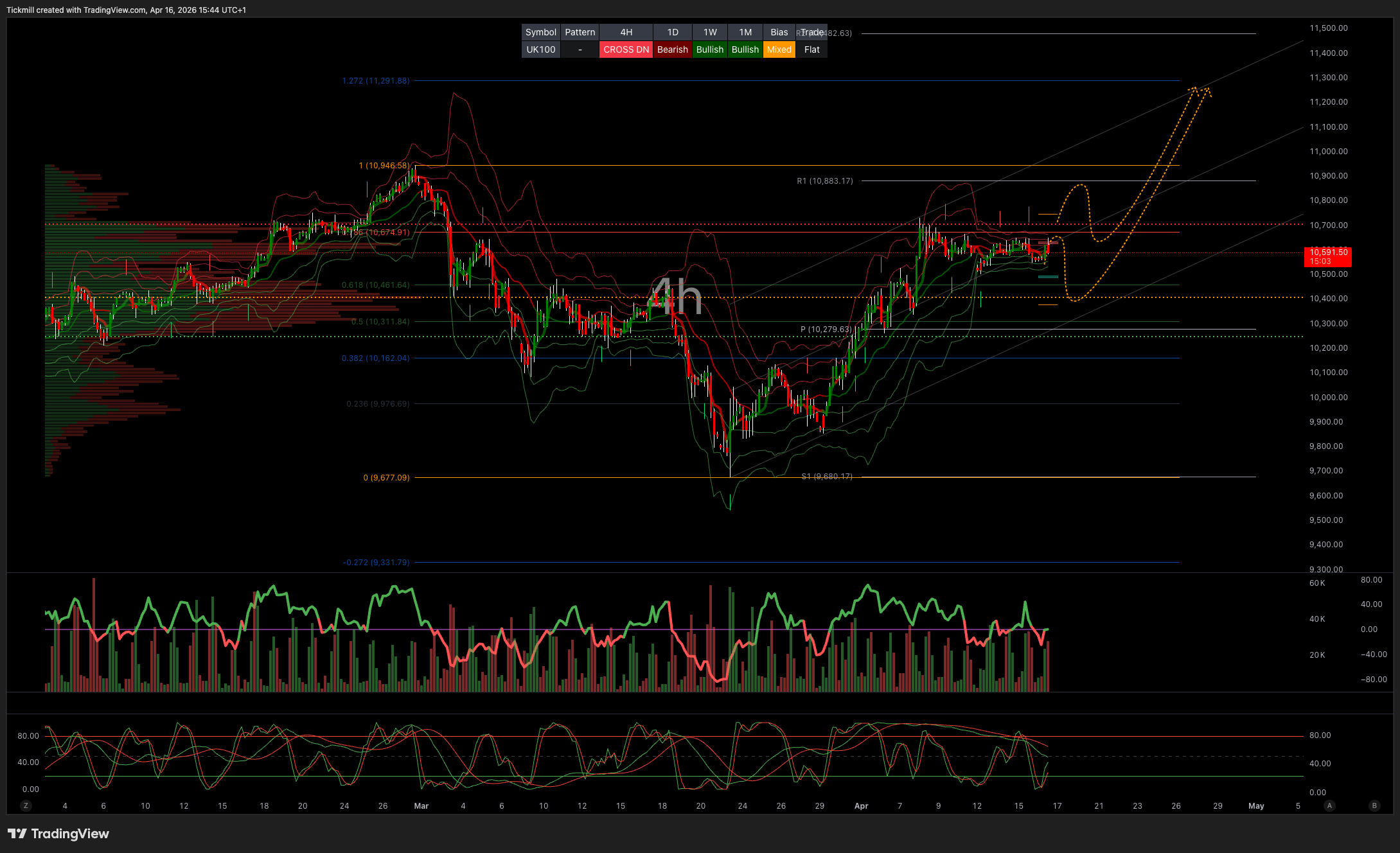

TECHNICAL & TRADE VIEW – FTSE100

Daily VWAP Bearish

Weekly VWAP Bullish

Above 10400 Target 11200

Below 10300 Target 10100

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!